We are pleased to provide you with a summary report on the performance of the WCM Quality Global Growth Equity Strategy (the Strategy) in January 2023.

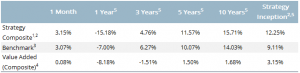

The Strategy1 delivered a return of 3.15% during the month, outperforming the benchmark MSCI All Country World Index return of 3.07%. The Strategy has delivered returns in excess of the benchmark MSCI All Country World Index over one month, five and 10 years, and since inception.

Notes: 1. WQG, WCMQ and WCM Quality Global Growth Fund (Managed Fund) have the same Portfolio Managers and investment team, the same investment principles, philosophy, strategy and execution of approach as those used for the WCM Quality Global Growth Strategy however, it should be noted that due to certain factors including, but not limited to, differences in cash flows, management and performance fees, expenses, performance calculation methods, and portfolio sizes and composition, there may be variances between the investment returns demonstrated by each of these portfolios and the WCM Quality Global Growth Strategy Composite (the Composite) in the future. As WQG, WCMQ and WCM Quality Global Growth Fund (Managed Fund) have only been in operation for a relatively short period of time, this table makes reference to the Composite to provide a better understanding of how the team has managed this strategy over a longer period. Performance is net of fees and includes the reinvestment of dividends and income. 2. Composite inception date is 31 March 2008. 3. Benchmark refers to the MSCI All Country World Index (with gross dividends reinvested reported in Australian Dollars and unhedged). 4. Value Added equals Composite Performance minus Benchmark performance. 5. Annualised.

The Strategy is conveniently available via four investment structures to accommodate the differing preferences of individual investors. You can read the full investment update for each of these products on the links below:

- WCM Global Growth Limited (ASX:WQG)

- WCM Quality Global Growth Fund (Quoted Managed Fund) (ASX:WCMQ)

- WCM Quality Global Growth Fund (Managed Fund) (Unhedged)

- WCM Quality Global Growth Fund (Managed Fund) (Hedged)

Strategy Update

Global equities made a positive start to 2023 with strong gains for both developed and emerging markets. Investor risk appetite rose in January following the sixth successive month of easing in US inflation and a relatively healthy annualised fourth quarter GDP growth rate of 2.9%. Positive developments in China boosted the local equity market and in turn emerging markets more broadly. Economic growth for the fourth quarter was higher than expected, with leading indicators such as subway passenger traffic turning upwards and regulatory pressure on the internet sector easing. Economic data from Europe provided further encouragement for markets. Reported GDP growth and leading indicators exceeded expectations and December’s Eurozone inflation print confirmed a further easing from 10.2 to 9.2%. Market leadership at a sector level during January came from those considered more economically sensitive such as Technology, Consumer Discretionary and Communication Services. At a regional level, emerging markets led by Chinese equities outperformed developed markets. The Australian dollar was stronger during the month, dampening returns for unhedged portfolios.

Stock selection contributed positively to relative performance of the portfolio in January with the largest contribution coming from holdings in the Consumer Discretionary, Health Care and Consumer Staples sleeves of the portfolio. Conversely, the largest detractors from a stock selection perspective came from the Industrials and Financials sectors. In terms of sector allocation, the portfolio’s underweight positions in Energy (zero exposure) and Consumer Staples added to relative performance. The main detractors were the above Benchmark positions in Health Care and Industrials and zero weighting in Communication Services.

The 2022 bear market in both bonds and equities has put significant pressure on the money management industry. Many industry participants have already announced reductions in head count and product closures. Investors familiar with WCM will be aware of the importance its investment team places on identifying companies demonstrating culture and economic moat alignment. Maybe less well known is how equally important this is for fund managers running their own firms. WCM’s response to the industry downturn reveals a lot about its focus on culture and moat expansion. Unlike most of its peers, WCM has continued to invest in people across all parts of the firm to grow its moat. This included adding to its team of culture analysts as referenced in WCM’s recent client letter: ‘Most importantly of all, we are doubling down on our culture focus. In 2022 we significantly expanded our team of culture-focused specialists with three new Business Culture Analysts, compounding our already strong lead in analysing companies’ culture from the key perspective of culture-moat alignment, culture strength and culture adaptability.’

DISCLAIMER: AGP Investment Management Limited (AGP IM) (ABN 26 123 611 978, AFSL 312247) is a wholly owned subsidiary of Associate Global Partners Limited (AGP) (ABN 56 080 277 998), a financial institution listed on the ASX (APL). AGP IM has prepared this material for general information purposes only for WCM Global Growth Limited, a listed investment company (ASX: WQG).

AGP IM is the responsible entity for WCM Quality Global Growth Fund (Quoted Managed Fund) (ARSN 625 955 240) (ASX: WCMQ) and WCM Quality Global Growth Fund (Managed Fund) (ARSN 630 062 047).

AGP International Management Pty Ltd (AIML) (ABN 33 617 319 123) is the investment manager for WQG and is an authorised representative of AGP IM. WCM Investment Management, LLC (WCM) is the underlying manager and applies its WCM Quality Global Growth Equity Strategy (the Strategy), excluding Australia, in managing each of WQG, WCMQ and WCM Quality Global Growth Fund (Managed Fund)(the Funds). WCM does not hold an AFSL. WQG and CIML are part of the AGP Group.

Any references to ‘We’, ‘Our’, ‘Us’, or the ‘Team’ used in the context of the portfolio commentary, is in reference to WCM Investment Management, as investment manager for the Strategy or CIML as investment manager for WQG.

Even though the Strategy, excluding Australia, is applied to each of WQG, WCMQ and WCM Quality Global Growth Fund (Managed Fund) certain factors including, but not limited to, differences in cash flows, fees, expenses, performance calculation methods, portfolio sizes and composition may result in variances between the investment returns for each portfolio. The performance of the Strategy is not the performance of the portfolios and is not an indication of how WQG, WCMQ and WCM Quality Global Growth Fund (Managed Fund) would have performed in the past or will perform in the future.

The material should not be viewed as a solicitation or offer of advice or services by WCM, AGP or AGP IM. It does not contain investment recommendations nor provide investment advice. It does not take into account the objectives, financial situation or needs of any particular individual. Investors should, before acting on this material, consider the appropriateness of the material.

Neither AGP IM, AGP, their related bodies corporate, entities, directors or officers guarantees the performance of, or the timing or amount of repayment of capital or income invested in the Funds or that the Funds will achieve its investment objectives. Past performance is not indicative of future performance.

Any economic or market forecasts are not guaranteed. Any references to particular securities or sectors are for illustrative purposes only and are as at the date of publication of this material. This is not a recommendation in relation to any named securities or sectors and no warranty or guarantee is provided that the positions will remain within the portfolio of the funds. Any securities identified and described are for illustrative purposes only and do not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Investors should seek professional investment, financial or other advice to assist the investor determine the individual tolerance to risk and needs to attain a particular return on investment. In no way should the investor rely on information contained in this material.

Investors should read the Product Disclosure Statements (PDS) of the Funds or any relevant offer document in full before making a decision to invest in these products.